Jan 26 - Welcome to the home for real-time coverage of markets brought to you by Reuters reporters. You can share your thoughts with us at markets.research@thomsonreuters.com

JUST DO IT ALREADY FED (1215 EST/1715 GMT)

While volatile markets have suggested investor jitters ahead of Wednesday's Federal Reserve statement, JonesTrading Chief Market Strategist Michael O' Rourke seems more anxious about what he believes the Fed won't do, rather than what he expects it will do, ie not much yet.

Register now for FREE unlimited access to Reuters.com

In a research note sent out late Tuesday, O' Rourke says the FOMC will probably announce it is holding policy steady, but it will set the stage for a March hike and an end to tapering.

However, O' Rourke complains that a delay of "the necessary and inevitable" will only serve to "leave investors in market limbo for the next 6 weeks until the March meeting."

Ahead of a tightening cycle, he says there is no rush for investors to further commit to an expensive market.

"It is hard to envision the end of a process that has not started and therefore, uncertainty abounds," he writes.

And O' Rourke believes the "policy tightening cycle will be 9 months behind schedule if the FOMC waits until March to act."

But quick action today would re-establish "a modicum of credibility" and afford policy flexibility tomorrow, as per O'Rourke.

While the Fed has long held a policy of telegraphing its moves well in advance, the strategist maintains that the market would prefer "short bursts of meaningful active measures that it can digest and proceed onward from, as opposed to a long, drawn out and uncertain process."

"If the Fed were to take more aggressive action, the most likely tactic would be to accelerate the end of asset purchases almost immediately," he said, adding that, "to make a real statement that the central bank is serious about inflation, the FOMC could raise interest rates."

He reminds us that the FOMC has not surprised the market with a larger than expected Fed Funds increase since February 2000, but still O' Rourke says he has a "lingering hope" for a more aggressive Fed.

Of course, back then, the market peaked the following month in March, and then declined into a deep bear market.

(Sinéad Carew, Terence Gabriel)

*****

PRE-FED DATA SHOWS U.S. ECONOMY NEARING 'NORMAL' (1115 EST/1615 GMT)

Data released on Fed Wednesday provided welcome evidence that the U.S. economy continues to shake off the dust of the pandemic recession.

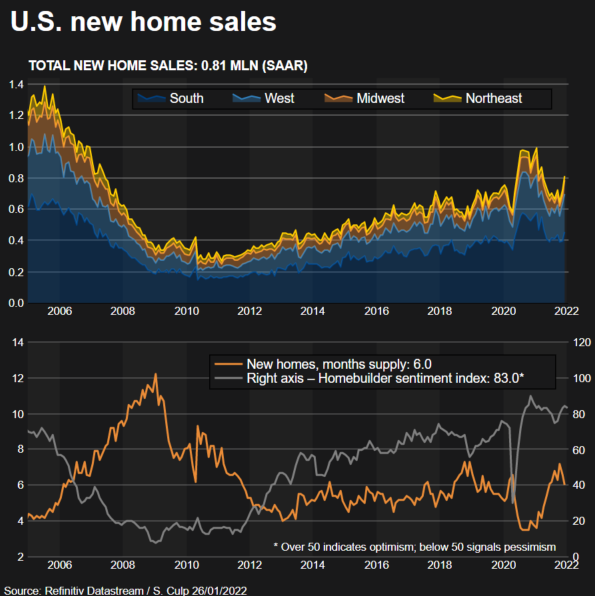

Sales of newly constructed U.S. homes (USHNS=ECI) surged by 11.9% in December, blasting past the 2.2% gain analysts expected. read more

That amounts to 811,000 units at a seasonally adjusted annualized rate, 51,000 units above consensus, rising again above pre-COVID levels.

It was a pleasant surprise, and combined with an upward revision of December building permits data - to 9.8% monthly increase from the previously stated 9.1%, bodes well for the homebuilding sector.

That sector has been supported by a dwindling supply of homes on the market amid a demand boom, but record low inventories and supply scarcity remain headwinds.

"Sales have undershot the pace implied by the path of mortgage applications in recent months, so a rebound was overdue," writes Ian Shepherdson, chief economist at Pantheon Macroeconomics. "We see scope for sales to rise further for the next couple months, but we then expect higher mortgage rates to bite in the spring."

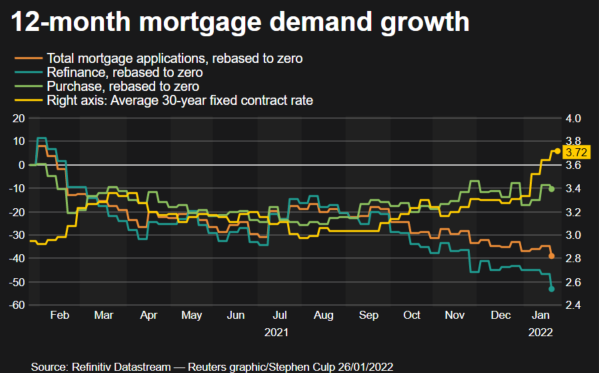

Speaking of which, rising interest rates sent demand for home loans plunging 7.1% last week, according to the Mortgage Bankers Association (MBA).

The average 30-year fixed contract rate (USMG=ECI) gained 8 basis points to 3.72%, in its fifth consecutive gain, reaching the highest level since March 2020.

This sent refi demand - which accounts for the bulk of total applications - down 12.6%. Applications for loans to purchase homes were off 1.8%.

"After almost two years of lower rates, there are not many borrowers left who have an incentive to refinance," says Joel Kan, associate vice president of economic and industry forecasting at MBA. "Of those who are still in the market for a refinance, these higher rates are proving much less attractive to them."

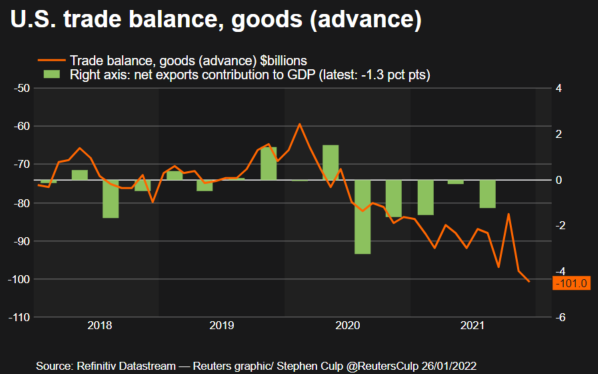

Finally, the busy Commerce Department issued its advance take on the goods trade balance and wholesale inventories for December.

The gap between the value of goods imported to the U.S. and domestic merchandise exported abroad (USGBAL=ECI) widened last month to $100.96 billion.

While imports and exports both increased, by 2.0% and 1.4% respectively, with imports' larger piece of the trade pie contributing to the widening.

"Trade flows will likely continue to be impacted by pandemic-related disruptions in the near-term," says Rubeela Farooqi, chief U.S. economist at High Frequency Economics. "But imports and exports should eventually rebalance as these effects diminish and global economies come back online more completely."

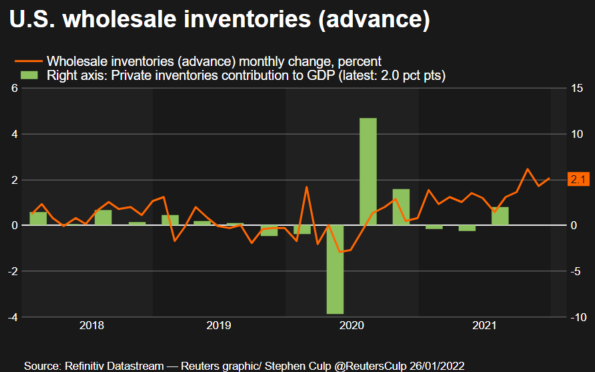

The value of goods stored in wholesaler warehouses (USAWIN=ECI) grew by 2.1%, building on November's upwardly revised 1.7% expansion.

Retail inventories, excluding autos, increased 3.6%, building on the prior month's 1.2% growth.

This bodes well for fourth-quarter GDP - the Commerce Department is due to take its first stab at that number on Thursday - and also suggests some steps toward normalization in the stricken global supply chain.

"Viewed in isolation, the trade numbers imply a small downward revision to tomorrow’s first estimate of Q4 GDP growth," Shepherdson says. "But the advance indicators report also shows that inventories of wholesale and retail goods both rocketed."

"Taking these data into account alongside the trade numbers, we are revising up our Q4 GDP forecast to 7.2% from 5.5%," Shepherdson added.

Wall Street burst from the starting gate into solid green territory at the opening bell, but those gains have since pared as zero hour approaches for the Federal Reserve's policy statement expected at 1400 EDT.

(Stephen Culp)

*****

WALL STREET OPENS HIGHER ON FED DAY (0953 EST/1453 GMT)

Wall Street's major averages are rallying on Wednesday morning and most of the S&P's 11 major sectors are in the green with technology (.SPLRCT) leading the charge as bullish corporate forecasts gave it a boost.

That said, while the bullish start may encourage some investors, if the intraday volatility of the last few sessions is any guide, anything could happen, especially in a session that will be bookmarked by a Federal Reserve statement after the conclusion of this week's FOMC meeting.

Meanwhile, investors are still keeping a cautious eye on Russia/ Ukraine tensions after Russia warned on Wednesday that imposing sanctions on President Vladimir Putin personally would not hurt him, but would be "politically destructive", after U.S. President Joe Biden said he would consider such a move if Russia invaded Ukraine. read more

However, earnings reports are definitely cheering up investors with Microsoft Corp (MSFT.O) gaining 5% after estimating current-quarter revenue broadly ahead of market estimates, driven in part by its cloud business and Chipmaker Texas Instruments Inc (TXN.O) is rising 3% as it also gave a positive outlook based on strong chip demand. read more

Here is your early trading snapshot:

(Sinéad Carew)

*****

S&P 500: ON TRACK FOR BIGGEST JANUARY DROP IN ITS HISTORY (0900 EST/1400 GMT)

Wednesday's results from the latest FOMC Meeting may be taking on added significance given that the S&P 500 (.SPX) ended Tuesday on track for its worst January performance in its history.

Indeed, the SPX is down 8.597% for the month, putting in on track for a bigger January slide than 2009's 8.566% tumble, which stands as the worst start to a year for the benchmark index using Refinitiv data back to early 1928. read more

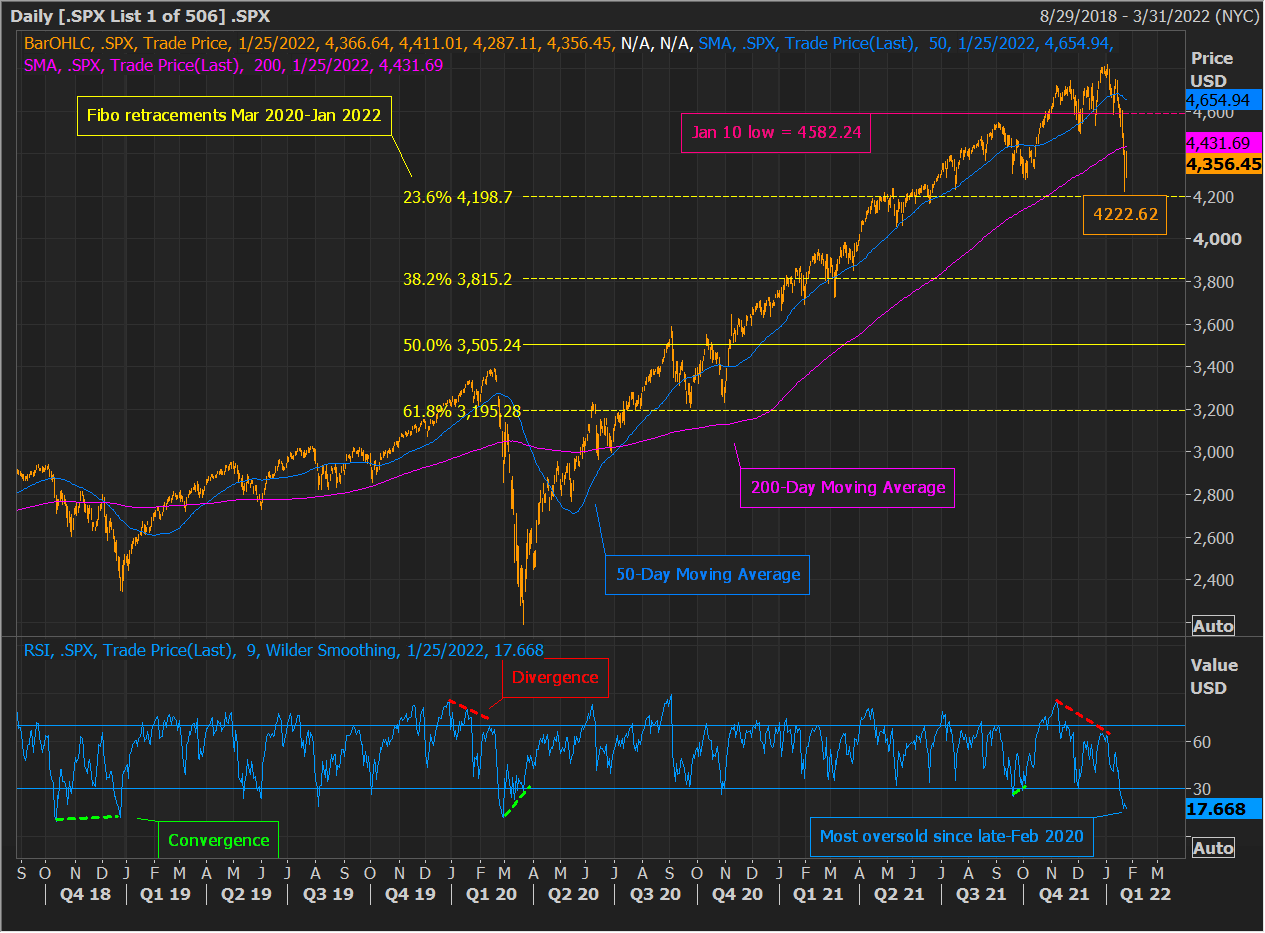

Meanwhile, based on the daily RSI, the S&P 500 ended Tuesday at its most oversold level since late-February 2020:

It now remains to be seen if this will prove to be a sufficiently washed out condition. Of note, since late 2018, the two most oversold readings on a daily basis, in October 2018 and February 2020, occurred in the early stages of declines. It was not until the SPX made new lows, coupled with a momentum convergence, that true bottoms formed.

If the SPX breaks Monday's low at 4,222.62, and the 23.6% Fibonacci retracement level of the entire March 2020-January 2022 advance, at 4,198.70, it can suggest risk for much more significant downside. The 38.2% Fibonacci retracement of the March 2020-January 2022 advance is at 3,815.20.

On strength, the 200-day moving average, which ended Tuesday around 4,432, presents resistance. The January 10 low, at 4,582.24, also looks to be a significant hurdle.

In the event of sudden upward reactions, traders will be assessing their structure, character and extent closely. This especially because, a CBOE Put/Call measure, which can be a considered a contrarian sentiment indicator, has broken out to 66.6%, or its highest level since May 2020 read more , and a number of market internal measures have yet to clearly stabilize. read more

(Terence Gabriel)

*****

FOR WEDNESDAY'S LIVE MARKETS' POSTS PRIOR TO 0900 EST/1400 GMT - CLICK HERE: read more

Register now for FREE unlimited access to Reuters.com

Terence Gabriel is a Reuters market analyst. The views expressed are his own

Our Standards: The Thomson Reuters Trust Principles.

"do it" - Google News

January 27, 2022 at 12:15AM

https://ift.tt/3o0QGxw

LIVE MARKETS Just do it already Fed - Reuters

"do it" - Google News

https://ift.tt/2zLpFrJ

https://ift.tt/3feNbO7

Bagikan Berita Ini

0 Response to "LIVE MARKETS Just do it already Fed - Reuters"

Post a Comment